Many financial planners are now recommending reverse mortgages, as they have finally begun to recognize the strategic uses of home equity as a retirement planning tool. Sadly, however, many will consider the product only once their other retirement funds are depleted. This “last resort” tactic has shown to be less than optimal in academic studies by Barry Sacks, Wade Pfau, John Salter, and others. When you begin to understand the dynamics of the federally-insured Home Equity Conversion Mortgage (HECM), you’ll find that waiting often doesn’t make sense.

WAITING SIMPLY DOESN’T PAY

In 2015, I wrote a piece titled Waiting Simply Doesn’t Pay. In the blog, I made the following statement:

“If you only have a basic understanding of Reverse Mortgages, then waiting appears to be the right advice. After all, older borrowers get more money, right? If I wait 5 more years, not only will I be older, but my home will be worth more, and I will have paid down my forward mortgage. These may seem like logical reasons to wait… to the novice.”

I went on to explain the following three reasons why it doesn’t pay to wait:

What I didn’t explain in my previous blog is that the costs and benefits of waiting are easily quantifiable.

WHAT IS THE INCREMENTAL BENEFIT OF WAITING ONE YEAR?

Even if the HECM program remains unchanged, and expected rates stay low (rounding to 5.0% or lower) in the future, the incremental benefit of the client being one year older, averages less than 1% more in principal.

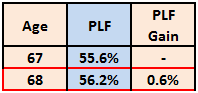

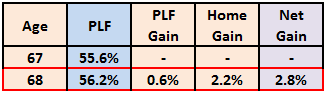

Consider a 67-year-old homeowner who wishes to wait another year when he or she is 68 years old. As you can see below, waiting one year would yield an increase in the homeowner’s calculated Principal Limit Factor (PLF) of 0.6%. Principal Limit Factors are tables, created by HUD, that determine how much a lender can offer a homeowner at the time the loan closes. In this example, a 67-year-old homeowner with a $200,000 home might have access to $111,200 at the time of closing. All other factors being equal, waiting one year yields this homeowner an increase of 0.6% or $1,200 more in principal.

Principal Limit Factors are tables, created by HUD, that determine how much a lender can offer a homeowner at the time the loan closes. In this example, a 67-year-old homeowner with a $200,000 home might have access to $111,200 at the time of closing. All other factors being equal, waiting one year yields this homeowner an increase of 0.6% or $1,200 more in principal.

If the home appreciates by 4% during this time, the homeowner would have access to 56.2% of that appreciation by waiting. Another way to express this is that a “home gain” would be another 2.2% (56.2% of the 4% increase).

This net gain of 2.8% is nice, but small when compared to the expected growth in the homeowner’s principal limit if they obtained the HECM at age 67 instead. This is because Principal Limits (for existing clients with adjustable rate HECMs) rise each year by the current interest rate plus 1.25%.

This net gain of 2.8% is nice, but small when compared to the expected growth in the homeowner’s principal limit if they obtained the HECM at age 67 instead. This is because Principal Limits (for existing clients with adjustable rate HECMs) rise each year by the current interest rate plus 1.25%.

At the time of this publication, a lender margin of 2.75% plus the 1-yr Libor index shows an initial interest rate of 4.522%. When 1.25% is added, the Principal Limit growth for the same borrower during that year would be estimated at 5.772% or $6,418.

Clearly, the PLF increase is small when delayed, and the borrower has lost some of the compounding potential of the product.

WHAT IF INTEREST RATES GO UP?

To determine a homeowner’s initial Principal Limit, we use “Expected Rates”, which is the market’s best estimate of future rates. As long as expected rates round to 5% or less, the borrower will receive the maximum principal limits for their age. In the example above, we established that a borrower at age 67 today can qualify for 55.6% of a home value of $200,000.

However, if long-term rates rise to 6% while waiting, this could yield the homeowner much less in principal.

A 1% increase in expected rates would probably drive the lender margins lower to stay closer to 5%. Otherwise, waiting one year could decrease principal limits from 55.6% to 43.6%. That is a reduction of 12% or –$13,344 in this example.

A 1% increase in expected rates would probably drive the lender margins lower to stay closer to 5%. Otherwise, waiting one year could decrease principal limits from 55.6% to 43.6%. That is a reduction of 12% or –$13,344 in this example.

Incidentally, if the HECM had been secured, any future interest rate increase could be beneficial, if that homeowner holds most of his/her funds in the growing LOC.

While we don’t want to create an unmerited sense of urgency, clients need to be aware that research shows that waiting for a reverse mortgage generally isn’t optimal. NOW may be the best time to obtain one.

For more information on the strategic uses for Reverse Mortgages, please subscribe to this blog and purchase my book, Understanding Reverse.

Dan Hultquist